Short memories protect our sanity. Dwelling on past mistakes makes us unhappy. The downside is that fiascos from the past are forgotten all too soon.

Forty years ago, August 1985 started like most other late-winter months in South Africa. Rain in the south; wind and dust storms in the north.

The only difference to normal weather patterns was a storm of expectations brewing about a looming speech by PW Botha, the then state president. At that time, South Africa faced increasing isolation, trade sanctions and sport boycotts. It was clear that the country urgently needed political change.

The economy showed the negative impact of international isolation. With disinvestment and continued capital outflow, the balance of payments and the exchange rate deteriorated. Gold and foreign exchange reserves were on the decline.

At the same time, South Africa was involved in an expensive war on the northern border of South West Africa, today the independent Republic of Namibia. Feeding the military machine was not only a drain on the fiscus but also took a heavy toll on human resources.

The border war was a drain on the fiscus. Most able-bodied young white men were called up for military service

A system of conscription supported the border war. Most able-bodied young white men were called up for military service. To many, this remains an unresolved puzzle. The National Party managed to run an extensive system of conscription in support of a largely secret war where young men were killed, but was nevertheless re-elected numerous times.

The country suffered exceptionally high inflation in the 1980s. The autonomy and independence of the Reserve Bank was in serious jeopardy after the “Primrose prime” incident. In November 1984, a few weeks before a parliamentary by-election (whites only, of course) in the Primrose constituency in Germiston, the central bank dropped rates, only to increase them again shortly after the by-election.

At the time, the FM stated correctly that “there is no escaping the fact that the cut in prime interest rates was most likely the opportunity cost of the National Party winning the Primrose by-election. Despite Reserve Bank governor Gerhard de Kock’s firm denial, this obvious political manoeuvre has all the signs of a quick fix.” Indeed, the increase in rates after the by-election proved the FM’s point.

The inflation rate had started accelerating from an already high level from the beginning of 1984. The acceleration in inflation and the decline in the rand exchange rate became a vicious spiral.

Change was inevitable. The status quo could not hold indefinitely.

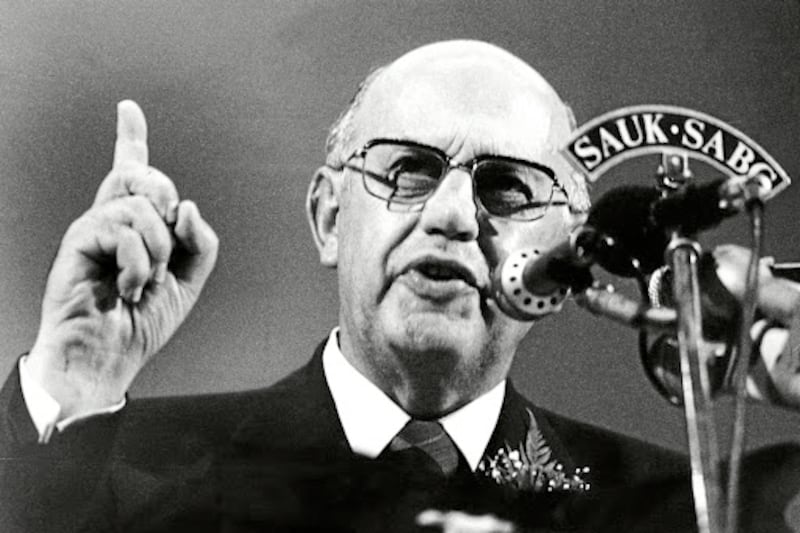

So, early in August 1985, rumours about the announcement of dramatic political changes started circulating. The occasion was to be a speech by Botha on August 15 1985.

Some strong calls for change came from within Botha’s National Party. To put it gently, he did not respond kindly to this internal pressure. Describing Botha as a stubborn man would be a mild explanation of his behaviour.

The speech became known as Botha’s infamous Rubicon speech. Mention was made in the speech to the defiant crossing of the Rubicon river by Julius Caesar in 49 BCE — indicating no turning back, an irrevocable decision. Caesar was starting a civil war.

Botha’s critics concluded that his own speech did not indicate any real constructive change in South Africa’s political or economic future.

The speech made things worse, because expectations — talked up by the likes of foreign minister Pik Botha — were dashed. It was followed by an acceleration in capital outflow. The sharp decline in the nominal and real (inflation-adjusted) exchange rates of the rand continued the trend from the end of 1983.

International investors followed old advice: if you want to panic, panic first.

The rand had been a stable currency for many years and many South African businesses had routinely borrowed abroad in foreign currency without forward cover. With the benefit of hindsight, it seems that increasing isolation made many South Africans oblivious to international financial risks.

Oblivious is used as a euphemism in this instance. The full impact of uncovered foreign borrowing amid a declining exchange rate soon became obvious as the rand value of foreign borrowing increased. Nedbank borrowed abroad on an uncovered basis for its own account and had to be bailed out by taxpayers.

After the Rubicon speech, international financial markets closed for South Africa. It was a turning point for the worse, as foreign credit lines were withdrawn. South African borrowers were unable to refinance their foreign short-term borrowing. A serious crisis was brewing.

On August 28 1985, the temporary closure of the foreign exchange market and the stock exchange was announced. On September 1 1985 South Africa announced a standstill on the repayment of its foreign debts. At the same time, exchange controls on South African residents and nonresidents were tightened.

The debt standstill was followed by debt rescheduling agreements. The final tranche of rescheduled debt was repaid only in August 2001.

Looking back on 1985, it is clear that the Rubicon was indeed crossed, but not in the way Botha might have envisaged. The financial sanctions and isolation that followed forced the South African government into negotiations for a new democratic political dispensation.

Speculating about different scenarios 40 years later adds little to the current debate. Botha’s crossing of the Rubicon in a positive manner would have made him a hero and would have ushered in much-needed political change.

Earlier change would have been at a lower cost to the South African economy, as the financial sanctions did considerable damage. By the time Nelson Mandela was released and talks with the ANC started in 1990, the National Party had not left itself with enough room to negotiate.

Never is a very long time, but it is unlikely that the events of August 1985 will be repeated in the next 40 years. This observation rests on a few conditions.

The Reserve Bank should retain its independence as enshrined in the constitution and should control inflation. Unnecessary wars and peacekeeping operations should be avoided. Political freedom with freedom of speech and media freedom should be protected.

It is perilous to forget events of the past and not to learn from them.

Rossouw is honorary professor at Wits Business School and economist at Altitude Wealth

Would you like to comment on this article?

Sign up (it's quick and free) or sign in now.

Please read our Comment Policy before commenting.